Act in Providing Effective Legal Support for Apartment Ownership & Management and Its Inconsistency with RERA (2016): A Comparative Analysis with the Maharashtra Cooperative Model")

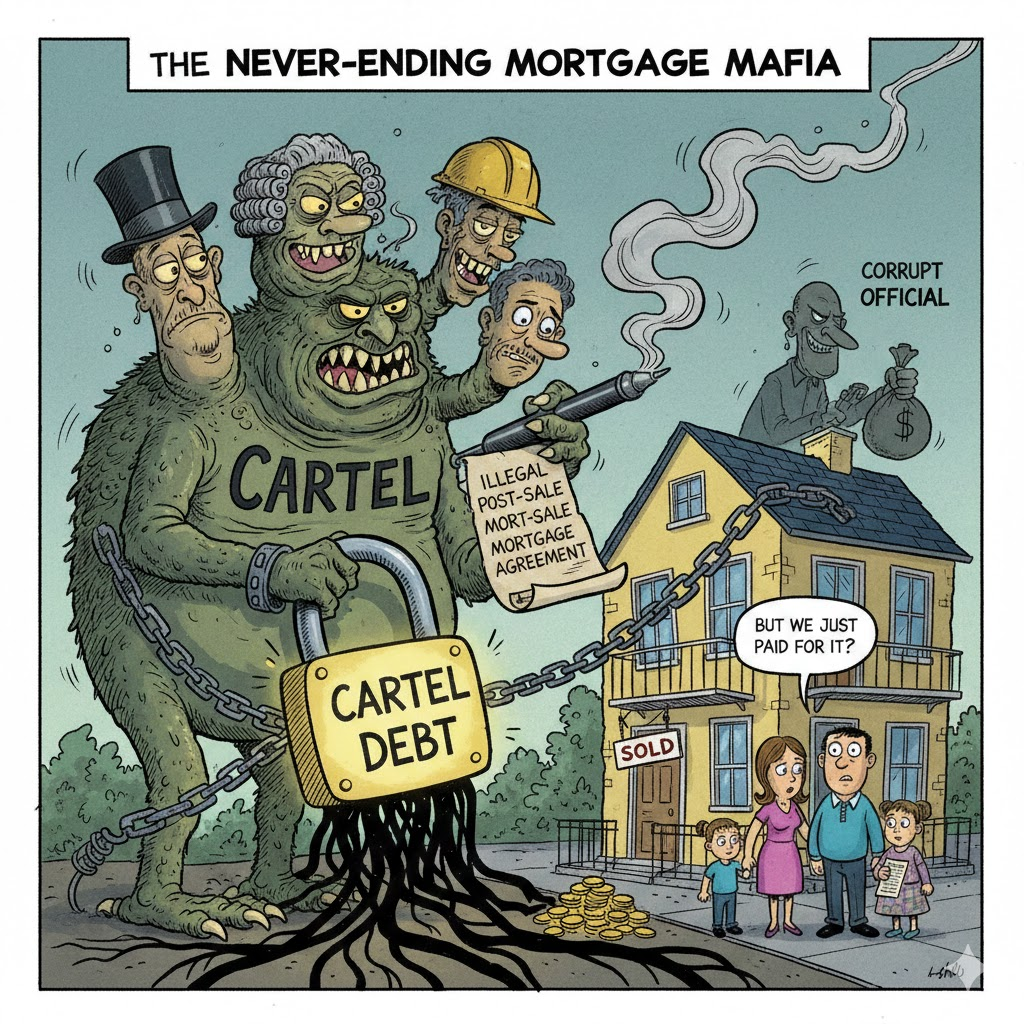

Builder–Bank nexus and the danger of Unregistered KAOA Accounts should be investigated by CBI & SC?

The Central Bureau of Investigation (CBI) and India’s higher judiciary have in recent months focused renewed attention on the relationship between real-estate developers and banks — a connection critics say has sometimes operated to the detriment of homebuyers. At the same time, watchdogs and legal commentators are warning about another problem unfolding alongside these probes: the use of unregistered apartment-association accounts under the Karnataka Apartment Ownership Act (KAOA) or similar informal bodies to hold and move crore-level funds — often run by entities that are neither registered nor recognised as consumer associations or juristic persons. Together these issues expose gaps in transparency, regulation and consumer protection across the housing sector.

What the CBI and courts have said so far

In late 2025 the Supreme Court authorised the CBI to register and investigate multiple matters alleging a collusive relationship between banks and developers in several cities, described in orders and press reporting as an “unholy nexus” in the use of subvention and loan disbursement schemes. The CBI told courts that certain subvention arrangements were allegedly misused, funds routed in ways that disadvantaged homebuyers and projects stalled while loans were advanced and repaid to builders rather than used for completion. The Court’s orders have expanded the CBI’s remit beyond the National Capital Region and permitted FIRs and preliminary inquiries into multiple projects and financial institutions.

Independent press reporting shows the CBI seeking land-allotment files, lease deeds and bank/payment records from development authorities for several large condominium projects as part of these investigations — underscoring that the probe is looking upstream at title, plan approvals and money flows, not only downstream symptoms like delayed possession. The allegations before courts centre largely on two mechanics frequently used in the sector:

- Subvention schemes (where banks advance or temporarily service EMIs while the developer completes the project); and

- Direct disbursements to developers after loan sanctioning, sometimes with inadequate escrowing or ring-fencing for construction.

- Non compliance of RERA Escrow accounts for the projects

Courts and investigators are scrutinising whether banks followed RBI/NHB guidelines on loan disbursement and whether developers diverted funds or used borrower money for other projects or purposes — conduct that, if proven, could trigger criminal, regulatory and recovery actions.

The parallel problem: unregistered “KAOA” accounts handling crores

A separate but related issue is the proliferation of unregistered apartment associations or informal “accounts” that hold large sums (crores) purportedly on behalf of residents, yet lack legal registration, clear governance, KYC transparency or juristic status. Recent commentary and legal analysis note that:

- Banks and financial regulations require that entities opening and operating accounts be identifiable and properly constituted; an unregistered association lacks the legal personality that standard KYC and corporate/association law assume. Regulators and legal analysts have warned that allowing such accounts to hold crores undermines traceability and accountability and creates money-movement risks that can attract the attention of enforcement agencies.

- Under consumer-law and the Consumer Fora jurisprudence, certain unregistered or foreign associations may lack locus (the legal standing) to file consumer complaints; similarly, an association formed under KAOA has specific requirements to obtain rights and responsibilities — absence of proper registration can mean the group cannot lawfully act as a “consumer” or as a juristic body for contracts and banking. This has consequences for who can sue, who can hold and disburse maintenance or corpus funds, and who is liable if funds are misused.

Where developers encourage or set up such unregistered accounts — whether for maintenance, corpus funds, or to collect buyer payments — the risk multiplies: funds may be controlled by individuals or informal committees, with limited audit trails, weak internal controls, and potential for diversion. Law commentators have flagged that such arrangements can be exploited to mask fund flows linked to developers’ wider business entities, complicating forensic accounting in cases where investigators examine whether buyers’ monies were diverted.

Why the two problems interact

The builder–bank nexus (alleged collusion around loans and subvention payouts) and the existence of large unregistered association accounts create overlapping vulnerabilities:

- Opacity at multiple points. Funds move from banks to developers, from developers to informal association accounts, and between multiple corporate entities — creating layered opacity that frustrates homebuyer oversight and investigator reconstruction.

- Weak legal standing for redress. If the body that claims to represent buyers is unregistered or lacks juristic status, its ability to sue, recover funds, or compel developer action (and to access regulator-mandated remedies) is compromised.

- Regulatory gaps and enforcement leverage. RBI/KYC rules, RERA orders and consumer forum jurisprudence all provide tools to close gaps — but enforcement requires paperwork, bank cooperation and inter-agency collaboration (CBI, ED, FIU-IND, RERA, state registrars), which is why courts have been pressed to expand investigative mandates.

Legal and regulatory stakes

If investigations substantiate misuse of subvention schemes or improper loan disbursal, consequences could include:

- Criminal prosecution under fraud/cheating and criminal conspiracy provisions (in cases where diversion or deliberate deception is proved);

- Regulatory action against banks for lapses in KYC or loan monitoring;

- Attachment or seizure proceedings if enforcement agencies (ED/FIU) find money-laundering links; and

- Civil remedies for homebuyers including refunds, damages, and orders for completion or possession subject to court/RERA directions.

For unregistered association accounts, legal remedies include requests that banks freeze or re-classify accounts, directions that corpus/maintenance funds be transferred to a registered juristic body, and consumer forum or RERA petitions seeking proper handover of finances and records. Regulators can also ask banks to strengthen account opening KYC for associations and require documentary proof of registration before accepting recurring high-value receipts.

Practical steps for homebuyers, banks and authorities

For homebuyers

- Insist on a registered apartment owners’ association (under the relevant law, e.g., KAOA or the Societies Act) with certified by-laws and audited accounts before transferring maintenance/corpus funds.

- Demand transparent bank statements, independent audits and receipts from a juristic entity (not a committee of individuals).

- Where possible, consolidate complaints through recognised consumer forums, RERA or court petitions rather than informal channels.

For banks and financial institutions

- Enforce KYC/documentation strictly for association accounts; require registration proof before permitting accounts that will receive large or recurring receipts.

- Apply due diligence on loan disbursements under subvention schemes and ensure escrows/escrow accounts operate as ring-fenced instruments tied to project progress.

For regulators and investigators

- Coordinate data-sharing between RERA, registrars (KAOA/corporate/coop), RBI, FIU-IND, and investigative agencies so money flows and titles can be reconstructed quickly. The Supreme Court’s orders expanding CBI’s investigative scope reflect courts’ view that a multi-agency approach is warranted.

The twin problems of alleged builder–bank collusion and the informal handling of crores through unregistered KAOA-style accounts are symptoms of a real-estate ecosystem that still permits dangerous opacity. The courts’ recent expansion of the CBI’s powers and legal commentary on the illegality and risks of unregistered association accounts together send a clear message: transparency, registration and strict KYC are not administrative niceties — they are essential protections for thousands of homebuyers whose life savings and housing dreams are at stake.

Builder–Bank nexus and the danger of unregistered KAOA accounts: CBI and the Supreme Court

The Central Bureau of Investigation (CBI) and Indian Supreme Court have in 2024–25 pulled back the curtain on what they call an “unholy nexus” between some banks, housing finance companies (HFCs) and developers — a pattern centred on subvention schemes, direct loan disbursements to builders and weak ring-fencing of buyers’ money. At the same time, Karnataka regulators and home buyers have exposed a parallel governance problem on the demand side: unregistered apartment association accounts (KAOA-style bodies or informal RWAs) holding and moving crores of rupees without juristic status, KYC transparency or clear accountability. Both problems multiply the risk to homebuyers and make forensic reconstruction of money flows much harder.

What the CBI and the courts are examining (and why it matters)

The controversy centres on subvention arrangements and related disbursement mechanics. Under many subvention schemes banks/HFCs sanctioned loans and made disbursements tied to milestones — or even paid amounts directly to developers while the developer ostensibly serviced EMIs until possession. Courts and the CBI have questioned whether (a) banks followed RBI/NHB norms about disbursal and monitoring, and (b) developers diverted sanctioned funds or used them across projects, leaving individual projects underfunded and homebuyers stranded.

The Supreme Court has authorised the CBI to convert several preliminary enquiries into registered cases and to probe multiple projects and banks in different cities — permitting the agency to file FIRs and widen its investigations into alleged collusion around subvention and loan disbursement practices. Why this is legally significant: if investigators prove diversion or deliberate misrepresentation, the conduct could attract criminal offences (fraud, cheating, conspiracy), regulatory action against banks for supervisory failures, and money-laundering/attachment proceedings by ED or FIU-IND. Courts have therefore allowed multi-agency evidence collection (RBI, RERA, development authorities, bank records) so that title, approvals and money flows can be reconstructed.

Recent orders and concrete examples

- The Supreme Court’s April 29, 2025 procedural order in the consolidated matters identified a large list of developers, HFCs and banks for closer inquiry and directed production of project files, payment records and details of subvention agreements to assist CBI/FIR registration. That order effectively broadened the investigatory lens beyond single projects to multi-city patterns.

- In late September 2025 the Supreme Court allowed the CBI to register six more cases arising out of homebuyers’ petitions alleging misuse of subvention schemes and collusion between banks and builders (the press has described the relationship as an “unholy nexus”). Reporting and court filings refer to dozens of projects and many banks across Mumbai, Bengaluru, NCR and other markets.

- Media and the investigative agencies’ follow-up show the CBI seeking land-allotment files, plan approvals and lease deeds from authorities (for example YEIDA in NCR) as part of a drive to link bank disbursements to project approvals and to determine whether sanctioned loans were used as intended. Supertech and other large-name developers have featured in reporting on the probe.

These orders show courts treating the alleged builder–bank collusion as structural — not isolated — and thus justifying broader evidence-gathering powers for central agencies.

Case law and legal principles to rely on

A few legal propositions and specific judicial touchpoints are particularly relevant when drafting petitions, curative pleadings or advisory memoranda for affected allottees:

- Supreme Court supervisory jurisdiction over multi-city frauds: The Court has, in recent consolidated interlocutory proceedings, directed coordinated investigations and allowed the CBI to register multiple RCs where prima facie evidence suggested systemic misuse of loan mechanics. (See the April 29, 2025 order and subsequent permission to file six additional RCs.)

- RBI/NHB supervisory standards and bank liability: Courts taking cognisance of these matters have asked RBI to place on record the instructions and supervisory norms issued to banks concerning subvention and escrow practices, thereby making it possible to measure bank conduct against regulatory expectations. Where banks ignore or circumvent RBI/NHB guidance, courts have been prepared to hold them accountable in connected proceedings.

- Multi-agency inquiry and money-trail reconstruction: Cases where courts have directed exchange of information among RERA, registration authorities and investigative agencies illustrate that relief in large-scale housing disputes often requires combining title/approval records with bank payment data — a point reflected in several recent orders allowing evidence production from local authorities (YEIDA etc.).

(If you want, I can extract precise paragraph/sentence citations from the April 29, 2025 SC order and draft suggested pleadings that cite the exact paragraph numbers.)

The parallel problem in Karnataka: unregistered KAOA bodies holding crores

While investigators examine upstream bank–developer money flows, Karnataka’s experience shows a downstream governance gap: unregistered apartment associations or RWAs that operate bank accounts and manage very large sums without juristic status or clear statutory backing. Courts and commentators have flagged multiple legal and practical problems:

- Lack of juristic status and enforceability — an unregistered body has weak legal standing to sue or bind third parties; under several Karnataka High Court decisions and RERA directions, associations that wish to exercise contractual or banking powers should be properly constituted/registered (for example, under the KAOA where appropriate). Recent Karnataka rulings have emphasised that association registration under the KAOA (or an appropriate statute) is often a condition to exercise certain legal rights and to be recognised by RERA and banks.

- Banking/KYC and RBI compliance — banks are required to conduct proper KYC and accept only appropriate documentary proof before allowing large, recurring receipts into association accounts. Commentators and banking-law analyses have argued that permitting unregistered KAOA-style accounts to collect crores violates the spirit (and sometimes the letter) of RBI guidelines and undermines traceability.

- Risk of commingling and diversion — where a developer encourages or effectively controls the informal association account (or where members are not empowered juristically), funds (maintenance, corpus, advance collections) can be commingled with developer accounts or used in ways that make forensic separation difficult — the very opacity investigators seek to unwind when they probe bank–builder links.

How the two problems interact — practical consequences

- Layered opacity: bank disbursements to developers + unregistered association accounts receiving large receipts create parallel, overlapping ledgers that are hard to reconcile. That hinders buyer remedies and criminal/forensic accounting.

- Weakened redress: an unregistered association may lack standing to file consumer or RERA petitions, or it may be easier for developers to resist handing over records — necessitating court directions even to obtain audited statements. Karnataka orders instructing that buyer bodies be properly registered reflect this problem.

- Regulatory leverage: multi-agency investigations (CBI, ED, FIU-IND, RBI, RERA) are now being used to pierce this opacity: the CBI’s access to project approvals and bank records, coupled with RERA’s records on allottee lists, creates a template for holistic investigations.

What relief the courts and agencies are prepared to grant

From recent orders and press reporting, courts/authorities have and can order:

- Production of bank records, loan sanction and disbursal memos, and subvention agreements; direction to banks and development authorities to hand over files to investigators.

- Freezing or attachment orders (in money-laundering or ED matters) where prima facie diversion is shown.

- Directions that maintenance/corpus funds be deposited into the accounts of a duly registered juristic body (KAOA-registered association or an appropriately registered cooperative/society) rather than an unregistered committee, together with audited accounts and transparency measures where necessary. Recent Karnataka/tribunal rulings support this approach.

7) Short practical checklist for affected homebuyers / advocates

- Demand written bank statements and audited accounts for any association account receiving maintenance/corpus funds; insist on transfer to a registered juristic entity.

- Where possession is delayed, preserve all loan sanction/disbursement letters, subvention agreements and receipts — these form the money-trail that investigators will need.

- File consolidated representations through registered buyer associations or ask courts to treat a representative petition as a public interest/interlocutory matter to trigger multi-agency data production. The recent batch of consolidated matters in SC provides a procedural template.

- If the association is unregistered, move for interim directions for audited statements and bank KYC proof — courts and RERA have been willing to compel this in Karnataka.

Conclusion — two fronts, one fight

The CBI and the courts are signalling that the housing-finance ecosystem will be examined end-to-end: from regulatory compliance by banks and HFCs, to developers’ use of sanctioned loans, to the legitimacy of downstream bodies that claim to represent buyers. For homebuyers, the immediate legal lessons are clear: insist on registration, audited accounts and documentary transparency; for advocates and agencies, the message is to coordinate evidence from RBI, banks, RERA and local land authorities so the suspect money trail can be traced and, where warranted, penal action taken

The most lethal weapon – three edged – The danger of subvention schemes along with diversion of loans direct disbursement to developers with out following needed norms & finally non adherence of. Rera Escrow accounts

Result : Huge bank money & EMI payees money getting diverted resulting in

in-complete & stalled projects (est 75 % as er RERA) which amounts to huge damage to

The interest of half . A-million home buyers & their 10 Lac crores investment in limbo for powsible “Bubble” at the cost of Banks (NPA) & half a million citizens who paid in crores with no shelter for years / even decade.

I agree with above stuiation and suffering from un registered associations collecting crores for completing builder responsible without any legal judgment. Even some lawyers had collided with these associations and acting as judges in Appartment amongst residents. Need you help .