Act in Providing Effective Legal Support for Apartment Ownership & Management and Its Inconsistency with RERA (2016): A Comparative Analysis with the Maharashtra Cooperative Model")

Fraud Behind the Facade: Bengaluru Real Estate, Illegal Mortgages, and the Regulatory Ripples in India’s Capital Markets

BENGALURU — As India’s real estate sector continues to attract institutional and retail capital, alongside a bullish stock market and rising private equity interest, an undercurrent of fraud and regulatory concern has begun to surface in Bengaluru’s property ecosystem. At the heart of this is a troubling practice: developers allegedly mortgaging already-sold apartments, diverting funds from buyer collections to other ventures or corporate needs — sometimes raising hundreds of crores without buyers’ knowledge or consent. While this issue is often discussed in property law forums and consumer complaints, its implications for capital markets, ethical finance, and securities regulation in India are seldom examined together. What happens when real estate developers and Bankers— some of which are publicly listed or connected to listed entities — misuse assets in a manner that could affect investor confidence, disclosures, and market integrity? This article investigates that intersection — real estate malpractice and securities regulation — and outlines the ethical, legal, and regulatory framework applicable under Indian law and SEBI’s mandate.

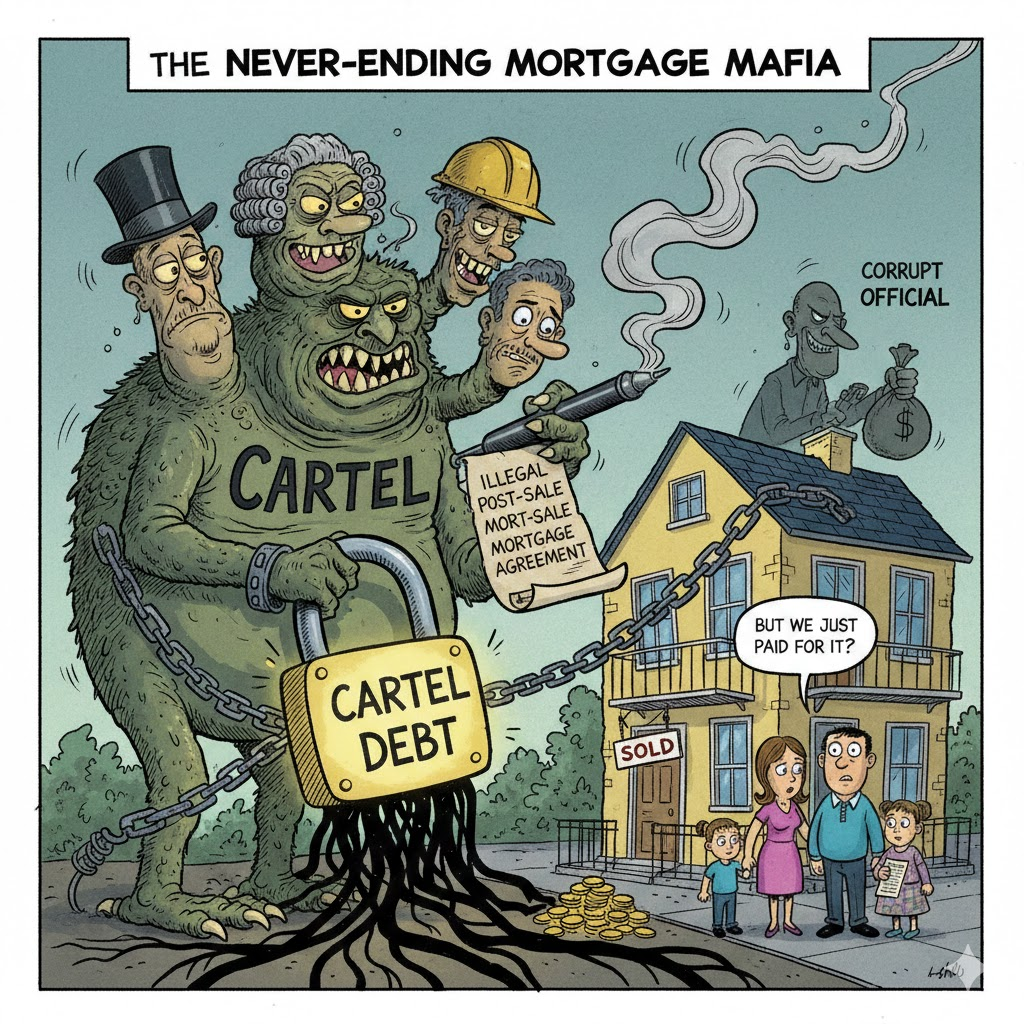

🕵🏽♂️ The Modus Operandi: Illegal Mortgaging of Sold Assets

Real estate developers typically sell apartments off-plan, receiving buyer funds long before construction completes. In a legally compliant scenario, these funds should be deposited into project-specific escrow accounts and used solely for that project. This is mandated by the Real Estate (Regulation and Development) Act, 2016 (RERA), which aims to protect buyer funds from diversion. However, enforcement gaps have allowed some companies to pledge already-sold units as collateral for loans, essentially using assets they no longer own free of encumbrance. Subsequent loan proceeds are sometimes deployed into unrelated businesses, land purchases, or even promoter compensation. After the sale the property is allowed to be managed by an unregistered non voluntary non-consumer entity under their control. These entities managed by the same builders long after the sale throw a blind eye on the illegal mortgaging and the BENAAMI in absence of effective laws to curtail it. The Judiciary also seems to be soft paddling these issues supposedly to encourage the development. This is not hypothetical. Individuals have reported discovering that their legally purchased flat is tied up in a lender’s mortgage long after sale and registration — leaving the buyer with uncertain rights and banks with complicated enforcement options. In other states, similar issues have resulted in police FIRs for cheating and criminal breach of trust under the Indian Penal Code (IPC). For instance, a case in Mumbai saw a real estate firm and its directors booked for allegedly cheating investors of over ₹31 crore, with charges including criminal breach of trust under the IPC. While specific Bengaluru cases tied directly to stock market abuses are not yet widely reported, the pattern of asset misuse and buyer deception has parallels in well-known national real estate regulatory action. Home buyers say that the complaints to the RBI, SEBI,Finance Department and other authorities have gone un-actioned. The Supreme Court has also empowered investigative agencies like the CBI to file and investigate multiple fraud cases against builders and banks in real estate scams, including in Bengaluru, showing that the judiciary recognizes systemic malpractices.

🕵🏽♂️ Why Is This a Stock Market Concern?

At first glance, real estate and stock markets might seem siloed — one physical, the other financial. But in India’s capital ecosystem, the risk spillover is profound:

1. Investor Trust and Market Confidence

The Indian capital markets rely on full and fair disclosure, which means companies must accurately report financials, liabilities, and off-balance sheet commitments. If a publicly traded developer or a company connected to listed entities diverts assets or raises funds covertly using already-sold flats, it could — in principle — lead to mis-representation of financial health or contingent risk. Regulators and investors treat such issues seriously because undisclosed encumbrances tied to entities with listed debt or equity can distort valuation, liquidity, and credit ratings of instruments such as corporate bonds — even though direct SEBI provisions target securities trades rather than property transactions.

2. Regulatory Framework: SEBI’s Mandate

Although SEBI (Securities and Exchange Board of India) primarily regulates securities markets, its Prohibition of Fraudulent and Unfair Trade Practices (PFUTP) Regulations and related securities laws have broader implications for fraud that indirectly affects market conduct:

- PFUTP Regulations: These prohibit any fraudulent, manipulative, or deceptive practices in relation to securities markets. Any misrepresentation or concealment of material financial information by a listed real estate company or affiliated entity could trigger action under these provisions if such conduct impacts share or bond valuations. These regulations mostly remain safely in the text books only to be referred when there is a hue and cry from the opposing parties.

- Disclosure Requirements: Under SEBI’s Listing Obligations and Disclosure Requirements (LODR), companies must disclose material events — including those that affect a company’s assets, liabilities, and financial condition. Hidden mortgaging of assets, once tied to loans or guarantees, is arguably material.

- SEBI Act, 1992 & Amendments: The Securities Laws (Amendment) Act, 2014 empowered SEBI to tackle Ponzi and illegal investment schemes more forcefully, including unregistered collective investment schemes often cloaked under property deals. This broadens the regulator’s reach beyond mere share trading.

Cases to Reflect On:

- Sahara India Pariwar: SEBI barred Sahara’s finance and real estate arms from raising money from the public because they mobilized thousands of crores via OFCDs without regulatory compliance. The Supreme Court later directed refund of over ₹24,400 crore to investors — demonstrating how securities law intersects with property money collection.

- Sai Prasad Corporation: SEBI barred this real estate conglomerate from collecting funds and ordered attachment of assets after determining unauthorized money mobilization.

These cases underline that when property money is treated as financial mobilisation subject to securities-market law, regulatory action follows. There are many more which don’t reach the Apex Court for action.

👉🏼 Legal and Ethical Grounds for Stock Market Action

While SEBI cannot directly prosecute property mortgaging under real-estate law, there are several ethical and legal bridges:

👉🏼 Misrepresentation & Non-Disclosure

If a listed real estate company fails to disclose that key assets are encumbered or that buyer funds are being diverted to other uses, it could run afoul of SEBI’s Listing Regulations and disclosure norms.

👉🏼 Related Party Transactions

Mortgaging 1000 of Crores sales inventory and lending funds to related entities without shareholder disclosure and without owners knoledge can be scrutinized as unethical related-party dealings under SEBI rules.

👉🏼 Market Abuse

Any financial strategy that leads to artificial valuation of securities — for instance by hiding liabilities or presenting healthier balance sheets — falls under PFUTP if it induces trading based on misleading information.

👉🏼 Enforcement and Penalties

SEBI has shown that it will impose penalties, bans, and reputational sanctions where needed. Recent actions include barring entities from markets and levying fines for misuse of funds and unfair trade practices. However, enforcement lags — partly because securities regulators have to prove material impact on investor decisions or trading behavior.

👮🏽♂️ Policy Recommendations and the Road Ahead

To bridge the gap between property fraud and market stability, India needs:

- Integrated Disclosure Regime: Link RERA and SEBI reporting so that asset encumbrances affecting public companies are automatically flagged.

- Stronger Escrow and Audit Enforcement: Mandate escrow audits tied into financial reporting for listed real estate firms.

- Criminal Penalties for Material Misstatement: Expand prosecutorial cooperation between financial regulators, police, and market intermediaries.

- Investor Awareness Campaigns: With SEBI’s investor protection mandate, targeted campaigns can warn retail investors about intertwined property securities risks.

The illegal mortgaging of sold apartments in Bengaluru and beyond points to deeper governance, enforcement, and regulatory coordination gaps. While RERA and criminal law address misconduct in property sales, India’s securities laws and SEBI regulations come into play when these malpractices affect market integrity, investor disclosures, and capital formation. Indian laws encompass every crime in the field but have failed to show results due to lack of implementation and accountability. Bringing these strands together not only protects home-buyers but safeguards India’s stock markets — ensuring that the confidence underpinning both property and financial assets remains well-founded.

Number of views: 326

This is not systematic failure. It is plain straight fraud and cheating by banks, RBI, judiciary, DC, Tahasildars, Police, CBI, EX

Under RTI, is SBI duty bound to answer a specific question…how many builders of residential apartments been granted mortgage loans based on the value of land in which the apartment complex was proposed to be built ?

Very nicely elaborated different aspects of frauds in real estate industry.